Economic Snapshot: Interest rate cuts arrive

February marked a turning point in Australia’s economic journey — the RBA made its first interest rate cut in over four years, a signal that inflation is gradually coming under control. While this doesn’t guarantee more cuts ahead, it’s a welcome sign for households and investors feeling the pinch of high rates.

Global markets had a mixed month through February. After a strong start to 2025, global equities dipped 0.4% in AUD terms. European stocks headed in a different direction, ending the month higher, rising 3.7% for an 11.4% gain year-to-date.

Meanwhile US markets lagged, generating a 1.4% outcome year to date, despite expectations of tech-driven growth and pro-business policies following the change of president. Policy uncertainty, including mixed messages regarding announcements and implementation of tariffs, added to investor uncertainty.

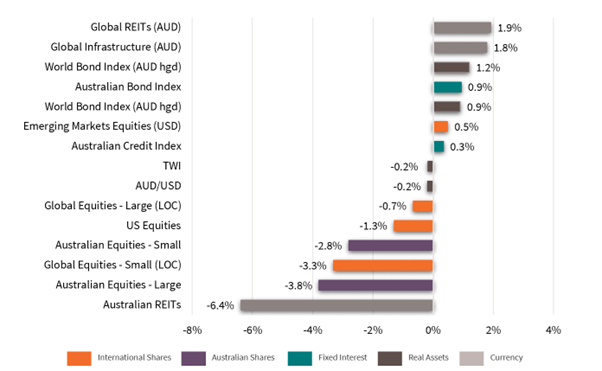

Closer to home, Australian equities dropped 3.8% in February, continuing to trail global markets. Over the past year, they’ve gained 9.9%. Bonds performed steadily, helping to offset some of the equity market negativity.

Global bonds rose 1.2% in February, delivering a 5% return over 12 months. Australian bonds gained 0.9% for the month and 4.2% for the year.

Chart 1: Asset Class Returns - February 2025

Source: Zenith Investment Partners Pty Ltd, Monthly Market Report, Issue 132, February 2025

Global Developed Equities

Global share markets hit a few speed bumps in February, especially in the US, where early optimism gave way to growing uncertainty about government policy and economic momentum. Europe, on the other hand, surprised to the upside.

After a strong start to 2025, global equities slipped 0.7%. Europe gained ground, rising 3.7% for an 11.4% year-to-date gain but the US lagged at just 1.4%, as expectations for tech-driven growth and a pro-business Trump agenda didn’t materialise. Instead, Europe’s recovery was driven by signs of economic stability, potential ECB rate cuts, and hopes for increased defence spending as peace talks in Ukraine progressed.

The US market fell 1.6% in February. Weak housing data, falling consumer confidence, and softer economic indicators pushed the Atlanta Fed’s GDP growth forecast to -2.8% for Q1. Policy uncertainty, including new tariffs and government workforce cuts, added pressure. Even a strong earnings and market update from Nvidia couldn’t reverse the downturn.

The Fed held interest rates steady at 4.25–4.5%, but weaker economic data led markets to expect three rate cuts over the next year. Bond yields fell to 4.21%.

Sectors like insurance, consumer staples, and REITs outperformed, while consumer discretionary, communications, and IT lagged. Value stocks outpaced growth, reflecting a shift in market sentiment. For investors, this month was a reminder that not all regions move in sync — staying diversified across global markets helps cushion against these swings.

Australian Equities

Back home, Australian shares lost ground in February despite hitting record highs earlier in the month. While the rate cut by the RBA was seen as positive news, it wasn’t enough to hold back the broader pullback.

The Australian equity market fell 3.8% in February, continuing to underperform global markets. The ASX200 hit record highs above 8500 ahead of the RBA’s rate cut to 4.1% on February 17 but slid afterward due to weak US economic data, tariff concerns, and rising uncertainty.

Banks dropped 4.6% after a strong run, though they remain up nearly 26% over 12 months. Healthcare fell 7.6%, IT 12.3%, and REITs 6.3%, while food and beverage stocks stood out with a 7.8% rise.

Economic data was largely positive. Retail sales saw their best quarterly growth since 2022, and the job market added 44,000 jobs in January, keeping unemployment low at 4.1%. The RBA expects unemployment to stay around 4.2% for the next two years, while core inflation is projected to fall to 2.7% by mid-year. This supports expectations of only modest rate cuts, with the cash rate unlikely to drop below 3.5% without any significant change to current expectations.

Australia has remained mostly unaffected by Trump’s tariff moves, but any escalation in US-China trade tensions could impact local growth and markets.

It’s normal for markets to have short-term ups and downs, especially as interest rates and global headlines shift. But over the past year, Australian shares are still sitting on solid gains — nearly 10% higher.

Emerging Markets

It was a tale of two markets in emerging economies. China powered ahead, while India and others struggled under pressure from global trade concerns and shifting investor sentiment.

Chinese equities surged 11.8% in February, driving a 39% gain over the past year. This reflects stabilising growth, market-friendly policies, and excitement around AI developments like DeepSeek, boosting Chinese tech stocks. While the US imposed new tariffs, they were lower than expected, and markets anticipate further fiscal support if tensions rise.

Elsewhere, emerging markets struggled. Indian equities fell over 11% in early 2025 as investors questioned high valuations, Korean stocks lagged despite a rate cut, and Indonesia dropped nearly 16% in February. Tariffs and global economic trends remain key themes for emerging markets this year.

Emerging markets can be more volatile, but they also present growth opportunities — especially in fast-changing sectors like technology.

Property and Infrastructure

Listed property had a tough month in Australia, driven by big names like Goodman Group and Scentre Group. Meanwhile, global property and infrastructure held up well, helped by falling bond yields.

Australian REITs fell 6.4% in the month. In contrast, global REITs rose 1.9% and global infrastructure also gained 1.8%, bringing its annual return to 15.8%, in line with global equities.

Property and infrastructure investments often move differently depending on location and market conditions, which is why spreading your exposure across geographies can enhance portfolio outcomes over the longer-term.

Fixed Interest – Global

In February, global markets faced growing uncertainty, driven by new US tariffs and softer economic data. The US imposed a 10% tariff on Chinese imports and announced 25% tariffs on Canada and Mexico, that were delayed until March. Additional tariffs on the EU and other trading partners were threatened, raising fears of a trade war.

US economic data painted a mixed picture. Job growth remained solid, with payrolls rising by 143,000 and unemployment falling to 4%, suggesting a normalised labour market.

However, consumer confidence, housing, retail sales, and corporate earnings weakened. The Atlanta Fed’s GDP growth estimate for Q1 dropped to -2.8%, pushing bond yields down to 4.21%.

In the UK, growth stalled, with inflation easing but still above target, limiting the Bank of England’s room for rate cuts. The Eurozone saw inflation at 2.5% year-on-year, but the ECB is expected to cut rates faster than the Fed and BoE to support growth.

Global bonds returned 1.2% in February, with investment-grade bonds up 6.2% over the past year and high-yield bonds gaining 11%. Markets remain focused on trade tensions and the potential for slower global growth.

Fixed Interest – Australia

The RBA cut the cash rate to 4.1% — the first cut in over four years — but signalled it was likely a one-off unless inflation falls further. January’s CPI data brought some reassurance, with headline inflation steady at 2.5% and underlying inflation rising slightly to 2.8%, suggesting inflation is gradually easing.

Retail sales showed strength, rising 1.4% in the December quarter, the best result since early 2022. Housing markets softened, with Sydney and Melbourne continuing to decline, bringing annual growth down to 4.3%. The labour market remained solid, adding 44,000 jobs in January, though unemployment edged up to 4.1%, mainly due to a higher participation rate.

Before the rate cut, markets expected over three cuts in 2025, but expectations dropped to fewer than two after the RBA’s cautious tone.

The Bloomberg Composite Index rose 0.9% in February, delivering a 4.2% return over the past year. Overall, the Australian economy shows resilience, though markets are adjusting to a more measured rate outlook.

Overall, bond markets quietly delivered some solid returns this month, helping balance out equity market losses. This highlights the value of fixed interest investments in a diversified portfolio, especially during uncertain times.

The RBA’s message was clear: they’re encouraged by the progress on inflation, but they’re not rushing into a series of rate cuts. For mortgage holders and income investors, this signals a period of gradual change, not a sharp turnaround.

Commodities and Currencies

Gold continued its run toward the US$3000 mark — not surprising in a world still dealing with conflict, inflation, and uncertainty. Oil fell on hopes for peace in Ukraine, while iron ore and copper rose, supporting Australia’s export outlook.

The Australian dollar remains volatile, bouncing around based on shifting interest rate expectations and global risk sentiment. That can affect travel plans, imported goods prices and some offshore investments.

Key takeaways for investors

- Rate cuts have begun, but slowly – the RBA has started easing policy, but don't expect a rapid return to ultra-low rates.

- Global markets remain mixed – regions like Europe are surprising on the upside, while the US and Australia face more uncertainty.

- Bonds are back – fixed interest investments are playing their traditional role as stabilisers in volatile times.

- Diversification remains a sound strategy – with ups and downs across regions and sectors, spreading your investments continues to reduce risk.

Looking for personal financial advice?

This investment update is a general overview of market movements for the month. For personal financial advice to achieve your investment goals, contact your FMD adviser.

If you're new to FMD, but ready to get serious about planning your financial future or a worry-free retirement, book an initial discovery meeting with one of our financial advisers in Melbourne, Adelaide or Brisbane.

General advice disclaimer: This article has been prepared by FMD Financial and is intended to be a general overview of the subject matter. The information in this article is not intended to be comprehensive and should not be relied upon as such. In preparing this article we have not taken into account the individual objectives or circumstances of any person. Legal, financial and other professional advice should be sought prior to applying the information contained on this article to particular circumstances. FMD Financial, its officers and employees will not be liable for any loss or damage sustained by any person acting in reliance on the information contained on this article. FMD Group Pty Ltd ABN 99 103 115 591 trading as FMD Financial is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977. The FMD advisers are Authorised Representatives of FMD Advisory Services Pty Ltd AFSL 232977. Rev Invest Pty Ltd is a Corporate Authorised Representative of FMD Advisory Services Pty Ltd AFSL 232977.